Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer LoginsEU passenger car sales up 6.0% y/y during March – ACEA

Passenger car registrations in the European Union have risen more slowly during March, albeit still up by 6.0% year on year (y/y) and helping to make further headway during the first quarter of 2016.

IHS Automotive Perspective

- Significance: Passenger car registrations in the EU have risen 6.0% y/y to 1.7 million units in March, helping to make further headway during the first quarter of 2016.

- Implications: Although the rate of growth has eased in March, the reasons for this are mostly technical due to Easter falling in March this year. However, when taking into account seasonally adjusted data, the trend remains strong with no real sign of abatement.

- Outlook: Although there are still risks, IHS Automotive currently anticipates that passenger car registrations for 2016 in the EU will grow by around 3.5% y/y to 14.2 million units.

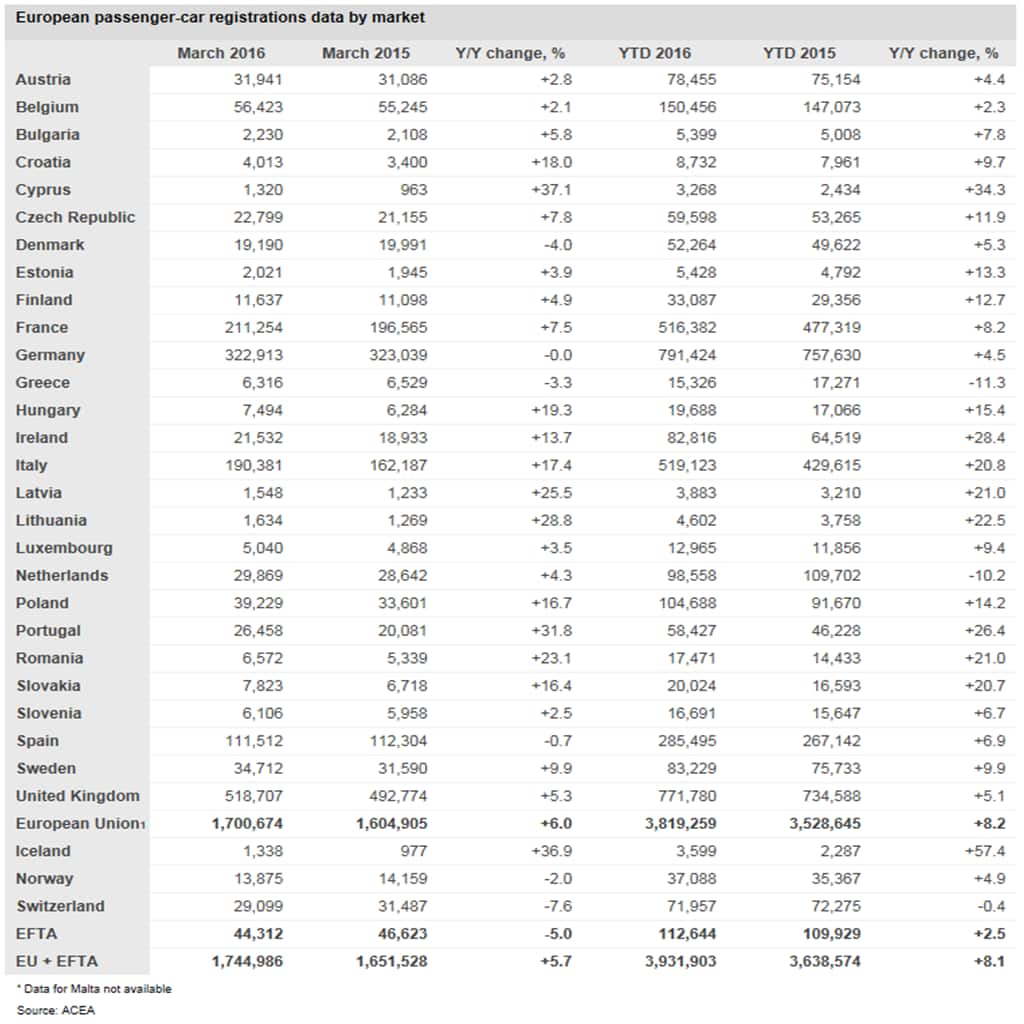

Passenger car registrations in the European Union (EU) have risen further during March, albeit at a weaker rate than earlier this year. According to data published by the European Automobile Manufacturers' Association (ACEA), demand has risen by 6.0% year on year (y/y) to 1,700,674 units, which has further contributed to its year to date (YTD), which for the first quarter now stands at 3,819,259 units, a gain of 8.2% y/y. Furthermore, in the European Free Trade Agreement (EFTA) area – Iceland, Norway and Switzerland – registrations fell by 5.0% y/y to 44,312 units, hurting its YTD which now stands at 112,644 units, an increase of just 2.5% y/y.

It has been a mixed month for the five biggest markets in the EU. The largest of these in March has been the United Kingdom as part of the biannual age-related number plate change cycle. Despite the significant growth during the past three to four years, the momentum is continuing and resulted in it setting a new monthly record of 518,707 units, which is also a gain of 5.3% y/y. Other gainers among this group this month have been France (+7.5% y/y) and Italy (+17.4% y/y), the latter benefiting from the growing replacement need amongst private customers as well as an incentive battle between key OEMs. However, the traditional leading market in the region, Germany, has flattened this month, while in Spain registrations have dipped by 0.7% y/y, although these weaker results are likely to be due to seasonal factors.

Outside this group, the market trend is predominantly gains, with plenty of these being double-digit percentage improvements. These include Portugal, Ireland and a host of markets in Central Europe and are continuing to record improvements on the relatively low base of comparison and a need for replacement. More stable markets such as Sweden and Poland have also recorded double-digit percentage gains. The Netherlands is also making a comeback after a relatively heavy decline in the first couple of months after it was hit by a tax change.

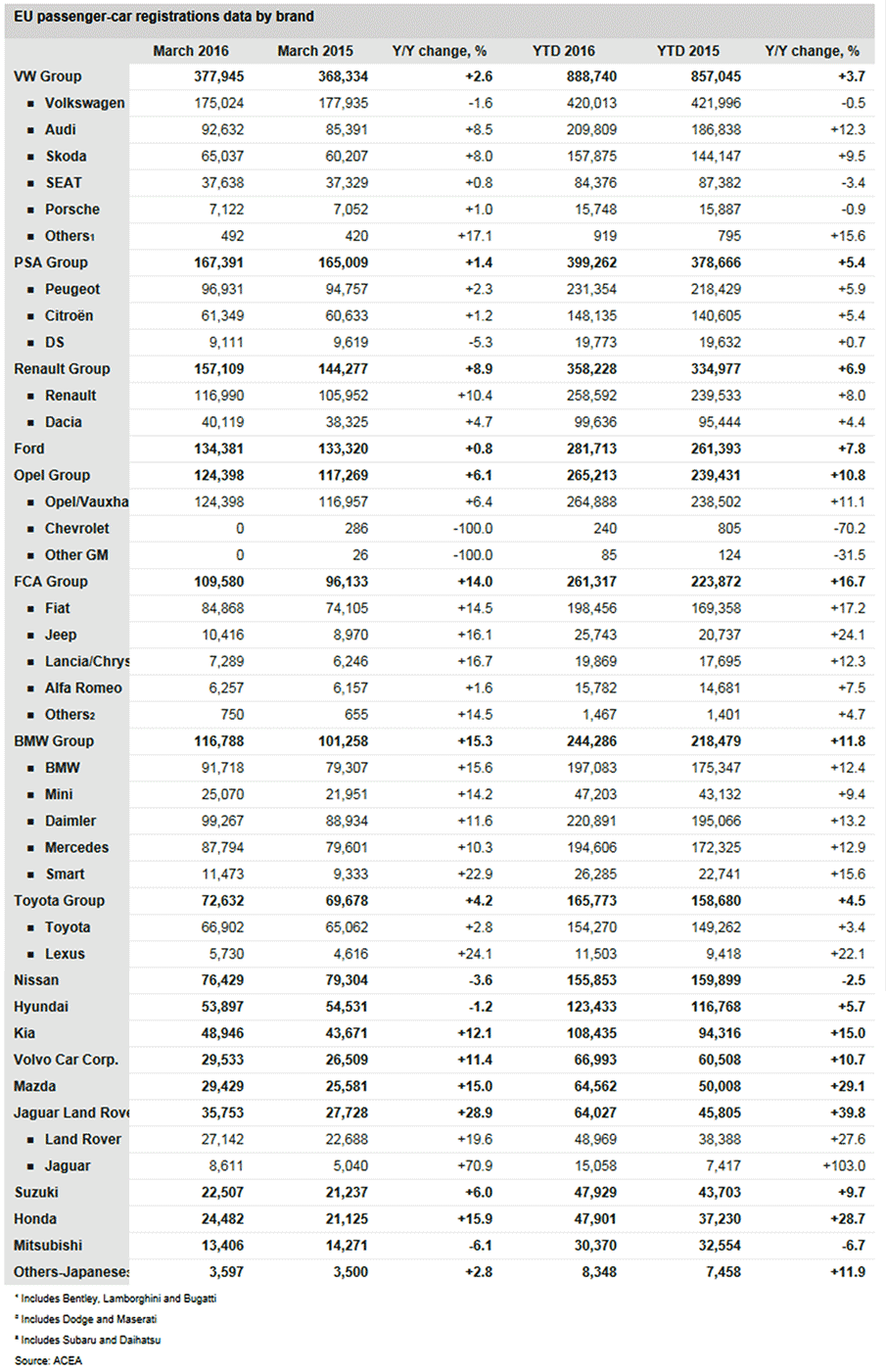

From an OEM perspective, the Volkswagen (VW) Group remains by far the market leader in the region in March, although its rate of growth is weaker than the wider market, at 2.6% y/y to 377,945 units. In terms of its brand performance it has been a mixed month for the automaker as well. Its namesake brand VW has fallen 1.6% y/y which may have been caused by the age of some of its key models and the impending launch of the second-generation Tiguan sport utility vehicle (SUV). It could also be some hangover from the impact of the negative publicity in to its diesel emissions. It has also been a weak month for SEAT with a gain of just 0.8% y/y, as it has not been helped by a slowness in its domestic market, Spain, and the age of the Ibiza. Nevertheless, it should be boosted later this year by the introduction of the new Ateca crossover. However, Audi has helped to offset this with a gain of 8.5% y/y, while Skoda is up by 8.0% y/y.

The situation with regards to other automakers in the region is equally mixed. Groupe PSA is the second largest OEM in the EU, but this month has struggled with growth of just 1.4% y/y to 167,391 units, as mild growth recorded by the Peugeot and Citroën brands has been partly offset by a drop in DS brand registrations. However, its local rival Renault Group has been far more buoyant as it recorded an 8.9% y/y improvement to 157,109 units, particularly lifted by its namesake brand's recent model launch offensive. Other OEMs to record significant gains this month have included Fiat Chrysler Automobiles (FCA) which has recorded a 14.0% y/y improvement to 109,580 units on new models and buoyant demand in the Italian market. Premium automakers have also achieved significant gains, including BMW Group (+15.3% y/y); Daimler (+11.6% y/y); Volvo Car Corp. (+11.4% y/y) and Jaguar Land Rover (JLR; +28.9% y/y), the latter also being helped by new entries in the market place.

Outlook and implications

Although the rate of growth has eased in March, Carlos Da Silva, manager of IHS Automotive's European light-vehicle sales forecast has said that it was not a big surprise. He explains that the reasons are mostly technical due to Easter falling in March this year and resulting in some markets posting far weaker sales. However, when using seasonally adjusted data the trend remains strong in with no real sign of abatement. In addition, he adds that the first quarter ended with growth on the strong side, which is particularly notable given that Q1 2015 was already when in to a recovery trend.

As for the wider picture, there is little change in the factors which are helping the region as pent up demand continues to be released in all markets, he added. While corporate and fleet sale activity remains the engine of growth in most markets, while greater support is coming from private buyers that suffered worst, such as Southern Europe. Da Silva adds, "Interestingly and hopefully, private demand seems on the verge of coming back also in those markets that were still shy on private demand - Germany, France - which is certainly indicative of better things to come." However, and unsurprisingly, tactical sales – those made to rental fleets and registrations by dealers and OEMs – have started to slow down which indicates less need to artificially sustain volumes.

Although these are positive hints for the remainder of the year, this does not mean that the risks have finally disappeared. Indeed, Da Silva notes, far from it. The global economy – and emerging economies in particular – still looks quite fragile, while in Europe, the influx of migrants and security crisis are still open questions, as is the integrity of the EU in general as the UK public are given the opportunity to vote on its membership in a referendum due to take place in June. Furthermore, Eurozone activity remains quite lifeless in absolute terms.

All in all, IHS Automotive assumes that, the current outlook for the EU passenger car market remains largely buoyant: on its current momentum alone, the market is headed for another very positive year. We currently see passenger car registrations for 2016 in the EU growing by around 3.5% y/y to 14.2 million units, with gains continuing to the end of the decade. Da Silva adds, "It will require a very bad event - or series of events - to derail the current trend, we think."

About this article

The above article is from IHS Automotive Same-Day Analysis of automotive news, events and trends, and is a deliverable of the World Markets Automotive Service. The service averages thirty stories per day and also provides competitor and country intelligence. Get a free trial.