Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer LoginsFuel for Thought: Automotive Scenarios for 2021 — The Virus and the Vaccine

Automotive Monthly Newsletter and Podcast

This month's theme: Automotive Scenarios for 2021 — The

Virus and the Vaccine

We have arrived at the crucible of the COVID-19 pandemic.

Containment measures are tightening to combat a more severe second

wave of the virus. Simultaneously, the availability of several

highly effective vaccines appears imminent. While not technically

mutually exclusive, these two key developments have very different

implications for the automotive industry. Our baseline outlook is

being squeezed between these two poles.

Policy actions implemented across major automotive markets have

supported growth, however, the future of many of these programs

remains in jeopardy. Successful clinical trials have reinforced IHS

Markit's expectation that effective vaccines will be widely

available to the general population in developed economies by

mid-2021. IHS Markit projects a COVID-19-induced decline in global

real GDP of about 4.5% year on year (y/y) in 2020, with the

sharpest contractions in Europe, India, and the Americas. Despite

rising COVID-19 infections, economic recoveries are now under way

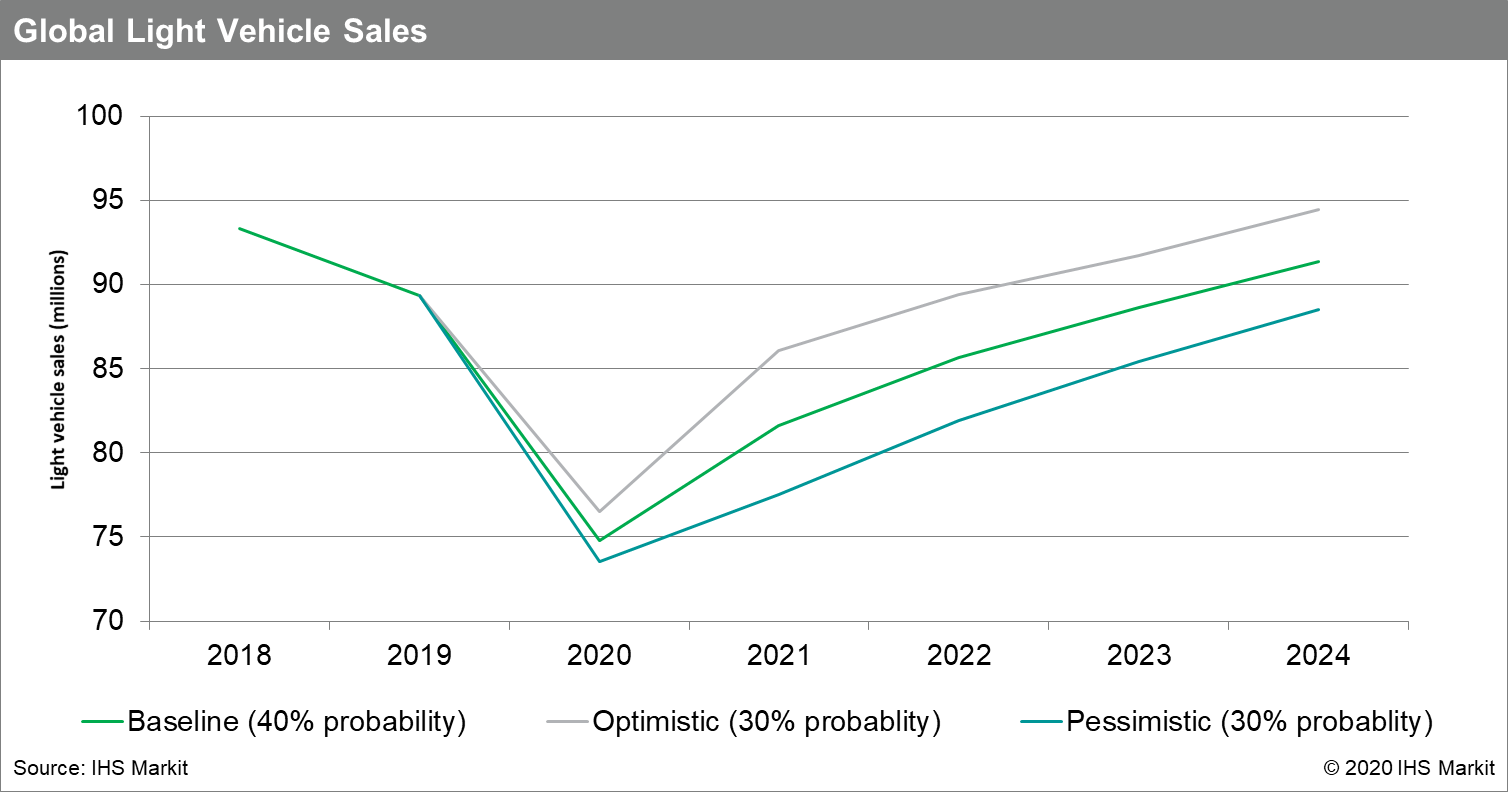

and will lead to global growth of 4.4% y/y in 2021. Light vehicle

demand will continue to pace the economic recovery. In our baseline

scenario, automotive sales grow 9% y/y in 2021, rising from under

75 million this year to almost 82 million in 2021.

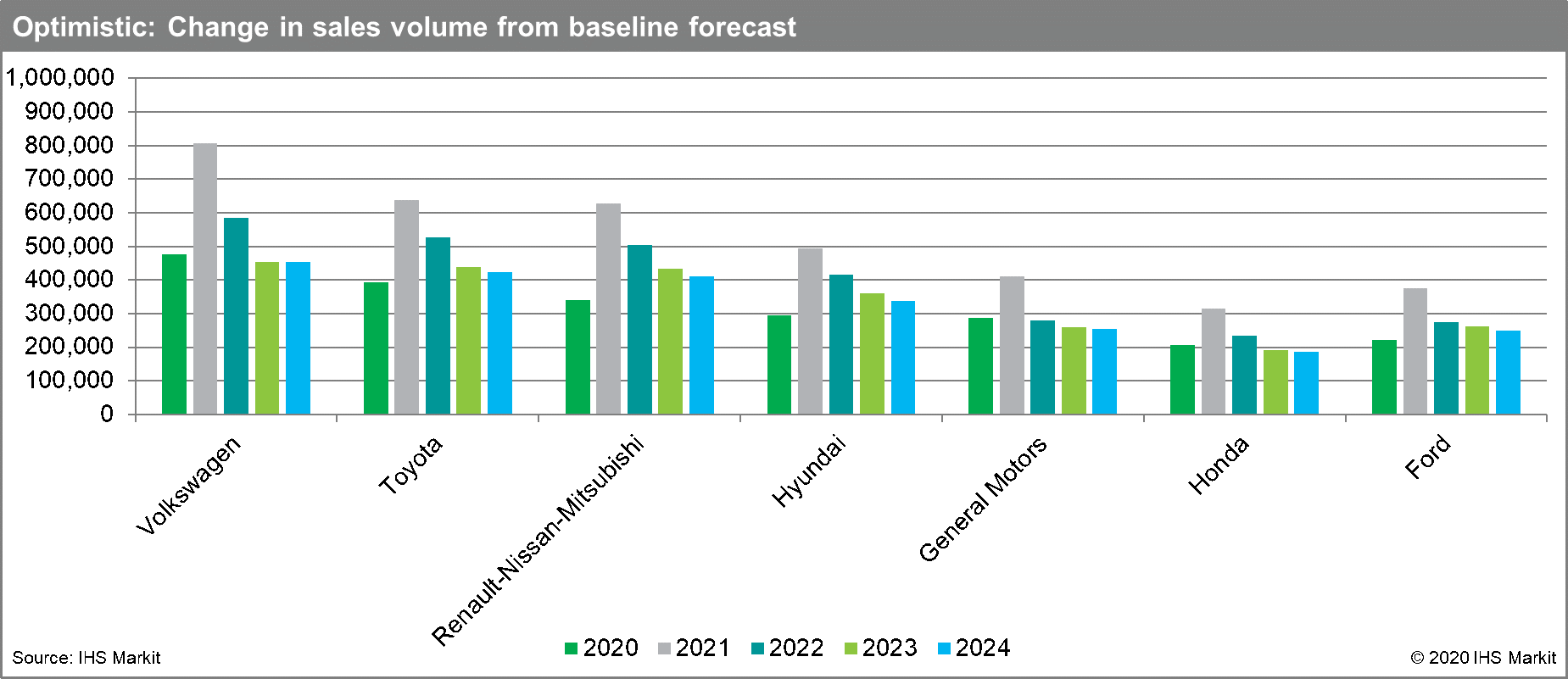

Optimistically, the COVID-19 pandemic appears to have boosted interest in private car ownership. Survey data from IHS Markit point to COVID-19 increasing demand for private car ownership in the United States, West Europe, and mainland China as first-time buyers expressed a need to reduce dependence on shared and public transportation. Health and safety concerns have elevated vehicle demand levels. Additionally, vaccine developments support near-term confidence in the recovery. Labor furlough schemes, income support programs, and government subsidies have supported a much sharper recovery in light vehicle demand; program extensions boost demand through 2021. In this scenario, which we give a 30% probability of occurrence, global GDP declines only 3.8% y/y in 2020 and rises sharply, 5.2% y/y, in 2021. Despite deep recessionary forces, the COVID-19 pandemic creates the unique possibility of consumers turning to car purchases for protection and mobility. A stronger economic response in 2021 accelerates the recovery in light vehicle demand. Global vehicle demand tops 86 million units, a 15.1% y/y improvement from the 2020 baseline.

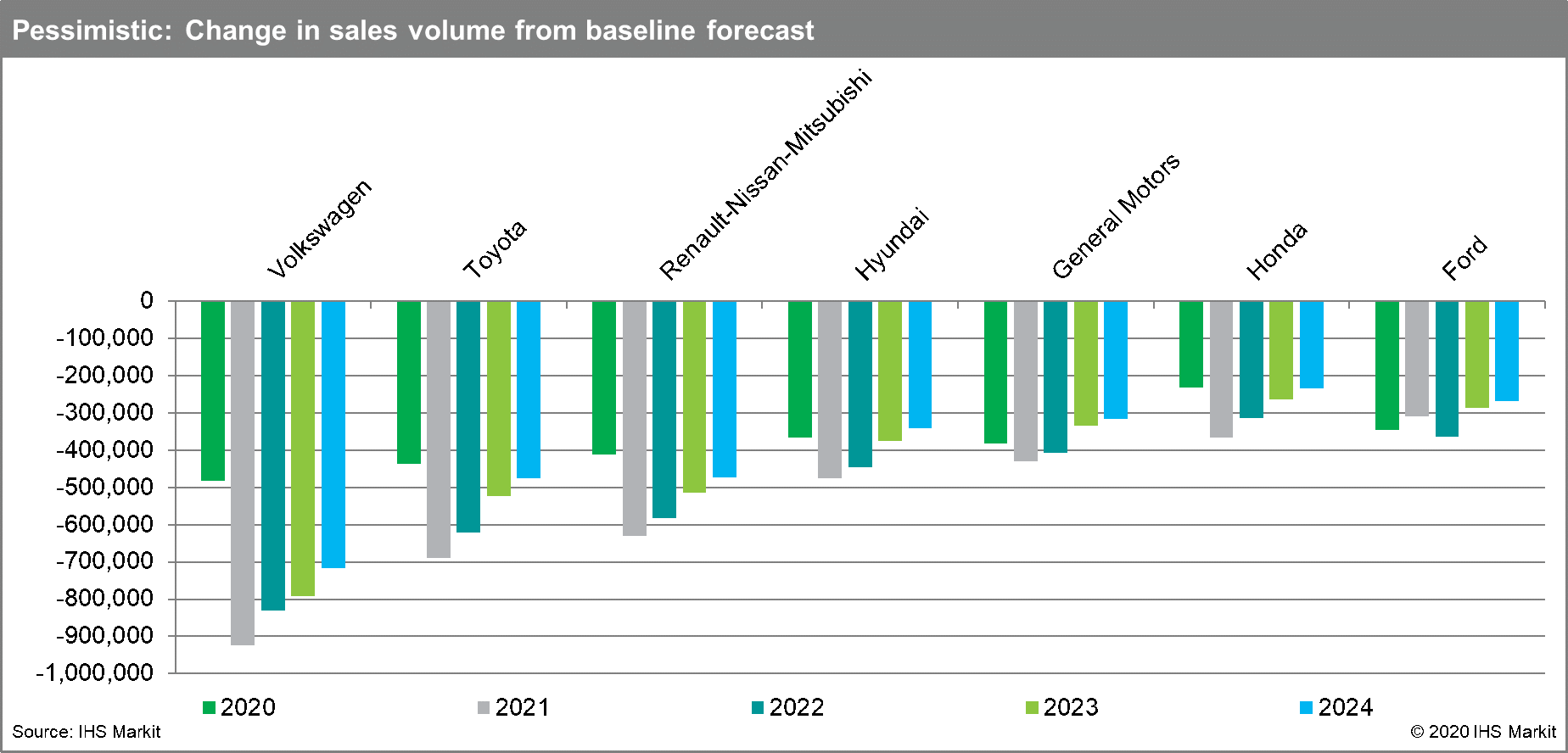

Conversely, a rising wave of new COVID-19 cases has resulted in large markets re-instating containment measures. Not only do these policies have a direct, short-term impact on automotive sales; they also create more lasting economic damage resulting in weaker future growth. High COVID-19 infection rates in the United States, Europe, and emerging markets such as India and Brazil create the risk of a global double-dip recession with a second downturn in the global economy by early 2021. Although this current phase of lockdowns is expected to be shorter and more flexible than measures implemented in the early 2020, failure to contain the spread of the virus will lead to further restrictions. Because of the worsening trajectory of global COVID-19 infections, we have given this more pessimistic scenario equal weight (30% probability of occurrence) as our optimistic outlook. In the pessimistic scenario, global growth collapses -5.4% y/y in 2020 and the economic recovery stalls in 2021 as GDP recovers only 2.6% y/y. Light vehicle demand recovers 3.7% y/y compared with the 2020 baseline as sales rise to only 77.5 million units in 2021.

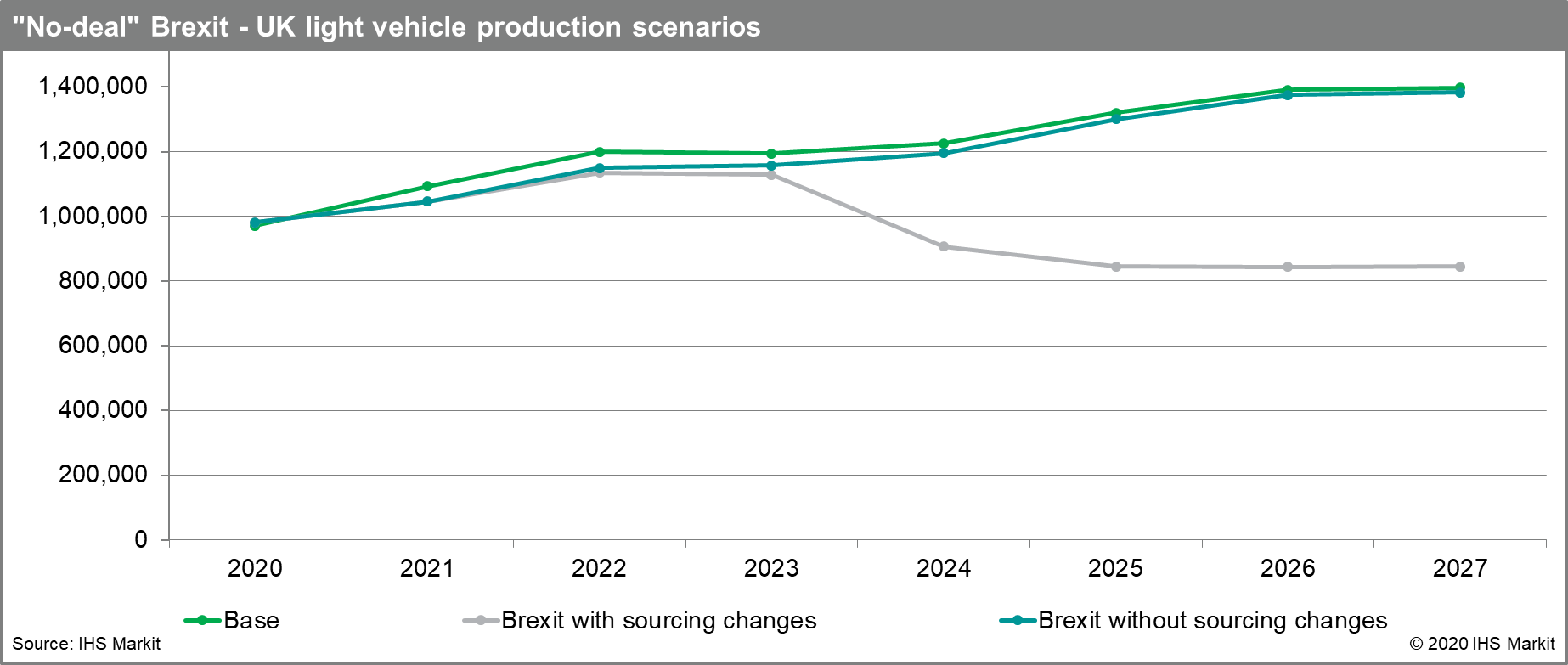

The threat of a "no-deal" Brexit has festered alongside the pandemic and the failure to secure a deal or an extension will result in drastic separation after 31 December 2020. "No deal" will have strategic repercussions on the automotive landscape on both sides of the English Channel. The next round of product investment across European facilities, particularly those in the UK, remains in jeopardy as global manufacturers pursue sourcing alternatives to avoid supply disruptions. Overall, "no-deal" Brexit volume losses are estimated at 0.75 million units in 2021, or 5 percentage points of growth. UK sales would suffer the full force of the failure to agree to a deal. On the other hand, UK production volumes and long-term sourcing potentially more exposed as "no-deal" conditions become entrenched. Other European nations, notably Germany and Turkey, could benefit from a reconfigured production landscape. Outside the region, countries such as Japan and Mexico would also benefit from increased trade frictions and, ultimately, Europe would be a net loser in total light vehicle production. Emissions regulations and local content requirements will result in higher vehicle prices across markets.

Dive deeper

What's in Store for Mobility in

2021?

Learn about our Contingency

Forecast add-on modules

Global Auto Demand

Tracker

New! Compliance+ Rolling Short-term

Forecast