Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer LoginsFuel for Thought - Market dynamics in the first year of the pandemic

Automotive Monthly Newsletter and Podcast

This month's theme: Market dynamics in the first year of the

pandemic

To say the least, 2020 was an unprecedented year for

the automotive industry. COVID-19 has accelerated developments in

the vehicle buyer journey that are sustainable beyond the first

year of the pandemic. Some companies were better positioned than

others to take advantage.

The year 2020 was an unprecedented year in terms of global auto

sales. Demand for new vehicles decreased 15%, to 73.8 million

units, in 2020 as a result of the COVID-19 pandemic. An estimated

USD355 million's worth of revenue stemming from sales of new

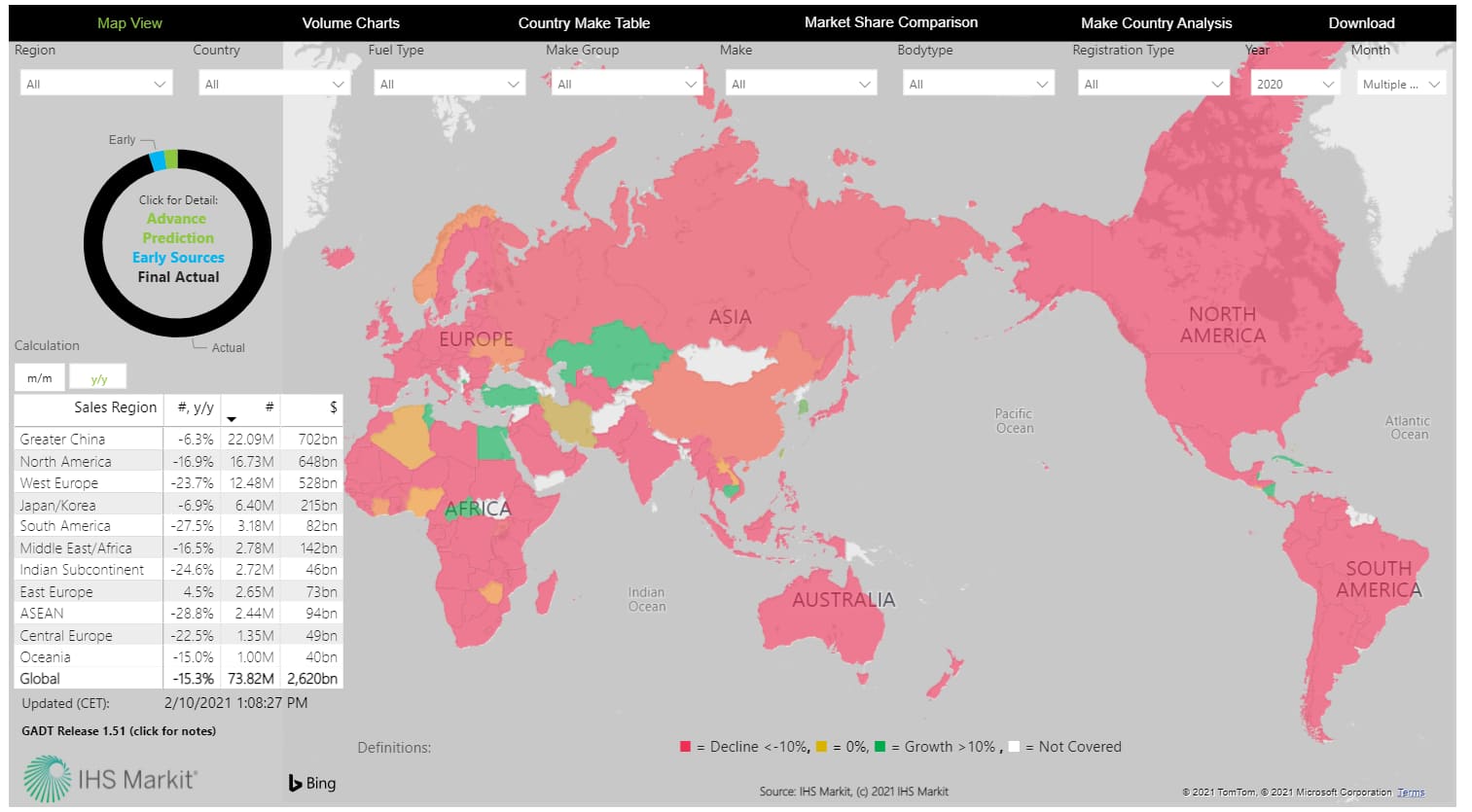

vehicles had vanished. As COVID-19 spread, IHS Markit released an

interactive dashboard called "Global Auto Demand Tracker", allowing

clients to quickly take the pulse of automotive sales — the

heat map below shows year-over-year growth by country (2020 vs

2019).

![]()

Mainland China: Volumes sharply declined, plunging to a seasonally adjusted annual rate (SAAR) of just 5.3 million units in February 2020, down from 20.7 million units in January 2020. As of May, the SAAR had somewhat recovered, trending at a 22.1-million-unit rate for 2020.

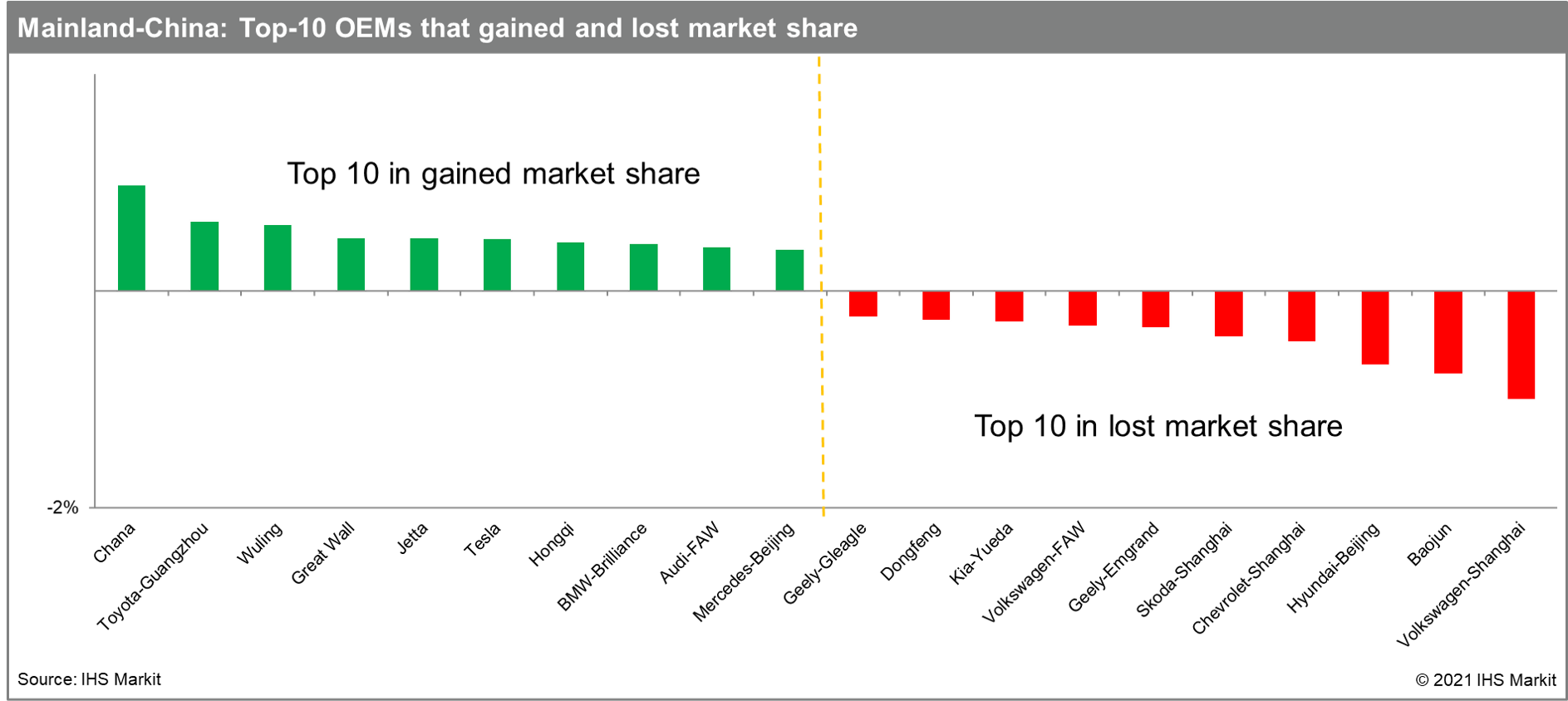

- While demand in mainland China was convalescing at a remarkable pace, other key automotive markets were still under lockdown, making a strong market position in mainland China paramount to recovery. In 2020, mainland China's share of global auto sales compared with the rest of the world increased from 27% to almost 30%.

- Winners of the crisis in mainland China in market share growth were volume brands, such as Chana, the joint venture of Toyota-Guangzhou, Wuling, and Great Wall. Equally noteworthy among the top-10 OEMs in terms of market share growth were premium brands such as Tesla, Hongqi, and the joint ventures of BMW-Brilliance, FAW-Volkswagen's Audi, and Beijing Benz's Mercedes, as the growing upper-middle-class Chinese consumers were turning to premium offerings.

- The share of new energy vehicles (NEVs), such as battery-electric vehicles (BEVs), plug-in hybrid electric vehicles (PHEVs), and fuel-cell vehicles, increased from 4.2% in 2019 to 5.5% in 2020. Specifically, NEVs were up in November and December 2020. To support the domestic automotive industry, mainland China's NEV subsidy scheme was extended to run through 2021 and into 2022, although with tightened technical criteria for eligibility.

![]()

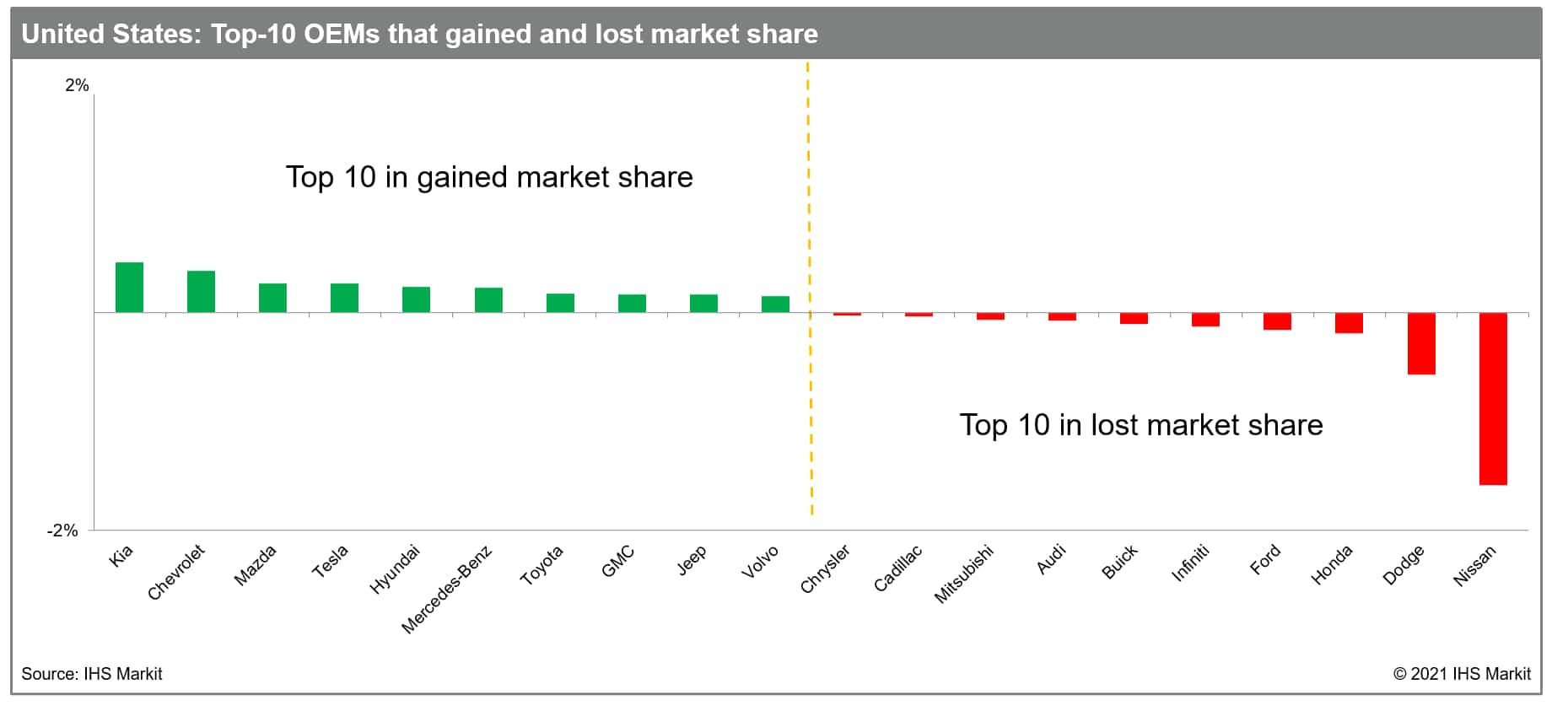

United States: Volumes were significantly under pressure during the pandemic. In April 2020, volumes were trending at a SAAR of just 10 million units. For the full year, volumes likely dropped 15.8%, to 14.2 million units, versus 2019. However, the reduction of the federal interest rate and the rollout of the largest stimulus program in history point to signs that the market is poised to start recovering once vaccinations start to ramp up. The widespread adoption and potential continuation of work-from-home schemes for much of the white-collar industries raise the question if there will be a permanent shift in the market dynamics after the crisis.

- In terms of electrification, the pace of transition to

e-mobility in the US has not been as significantly accelerated as

it has been in Europe. There have been introductions of new models

from volume manufacturers, such as Ford with its Mustang Mach-E,

into what has been until now a segment dominated by Tesla.

- The COVID-19 crisis resulted in not only economic conditions affecting customer demand for new vehicles, but on top of this also physical conditions restricting the traditional vehicle purchasing process and hence sales globally. Some automakers were in a better position to limit the damage directly from the start of the outbreak. Tesla adapted to the situation by offering touchless test drives as a "new default for zero-contact experience", introducing this concept first in mainland China and now across the globe, helping to build consumer trust in this period of uncertainty.

- Many traditional automakers have also reacted swiftly to help position themselves for a better recovery, with Stellantis's Drive Forward initiative now offering North American customers the option for a completely online retail experience, from trade-in to credit application, and approval to home delivery. The crisis has led to a new definition of the vehicle buyer journey across the globe, with ease-of-access, ease-of-purchase, and digital-first retail now at the forefront of many automakers' strategies.

![]()

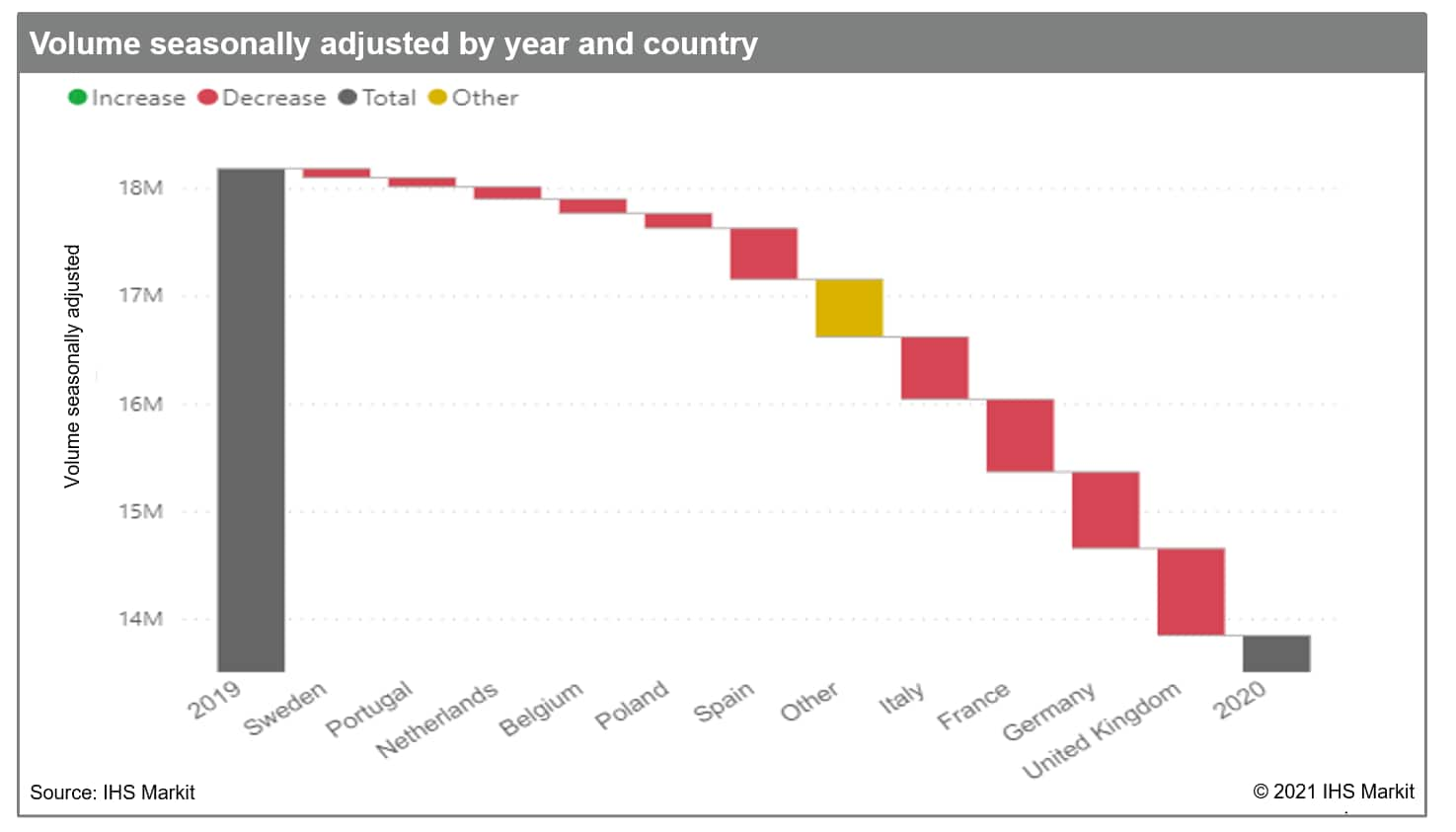

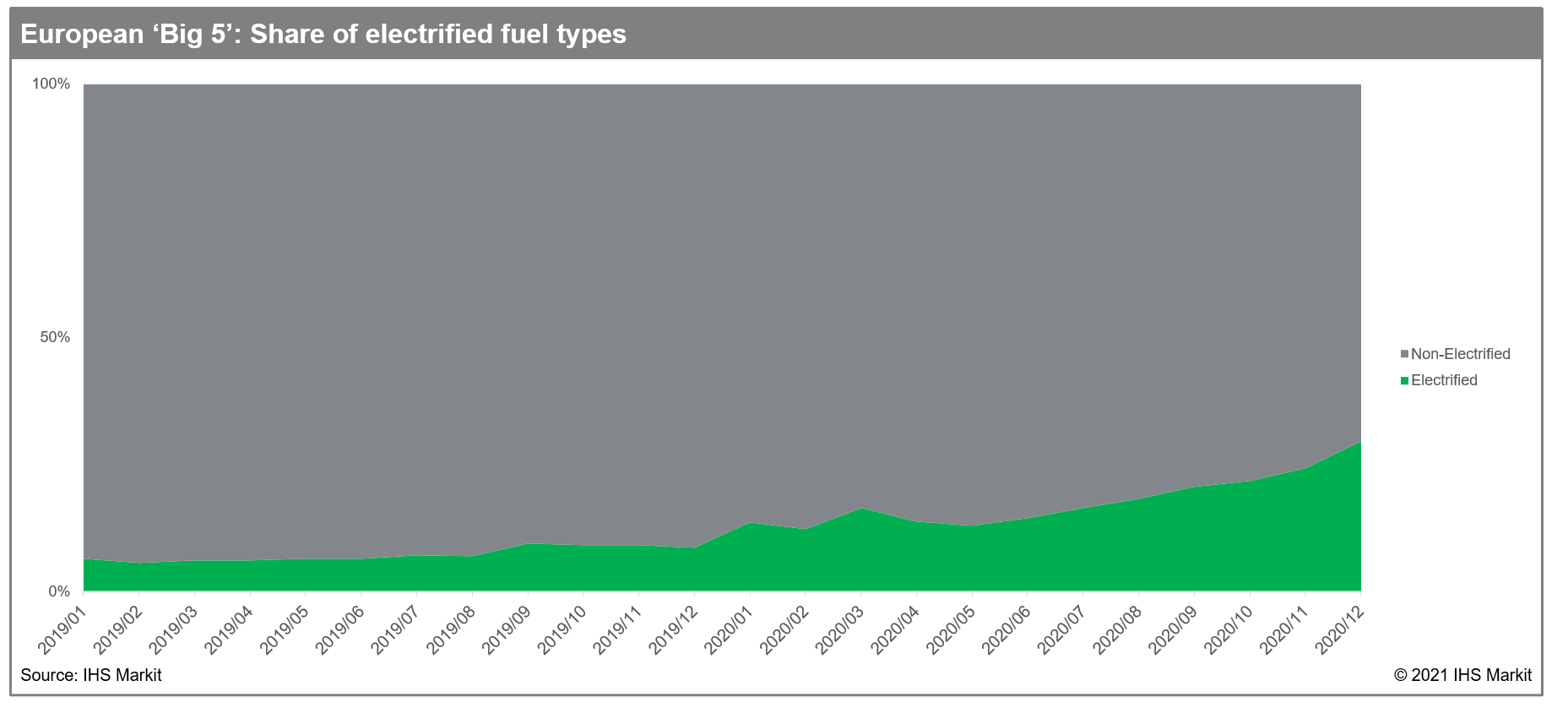

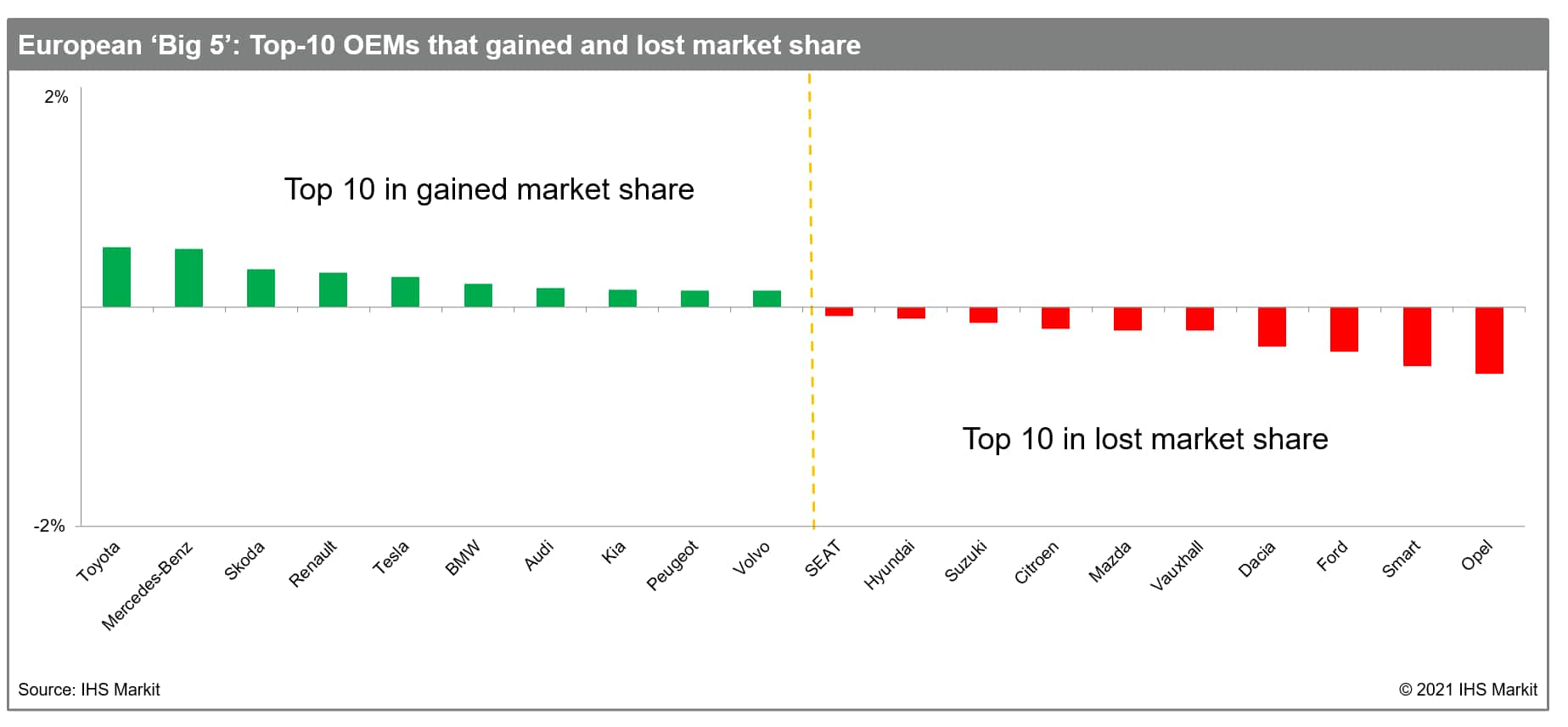

Europe: Central and Western Europe were among the hardest hit regions globally, as vehicle demand reduced by 4.3 million units, to 13.8 million units. Three-quarters, or 3.1 million units, of that loss were incurred by the European Big 5, notably Spain (-31%), the UK (-28%), Italy (-27%), France (-24%), and Germany (-19%).

- In midyear, various stimulus programs and incentives were launched in, for example, Germany, France, Italy and Spain. Aimed at spurring xEV adoption, these incentives helped to accelerate demand for electrified vehicles in the second half of the year. December 2020 was somewhat distorted by OEMs' own registration activity in a final push for carbon dioxide (CO2) fleet compliance targets.

- Tesla did well in 2020 in Europe, with strong UK and European demand. However, the BEV space is becoming increasingly crowded, with more European brands going to market with their own offerings.

Dive Deeper

Global Auto Demand Tracker provides up-to-date vehicle sales numbers

Download Report - Understanding the Vehicle Buyer Journey

Learn more about EV charging infrastructure developments

Myth vs Reality - No longer speculation, the future is electrified