Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

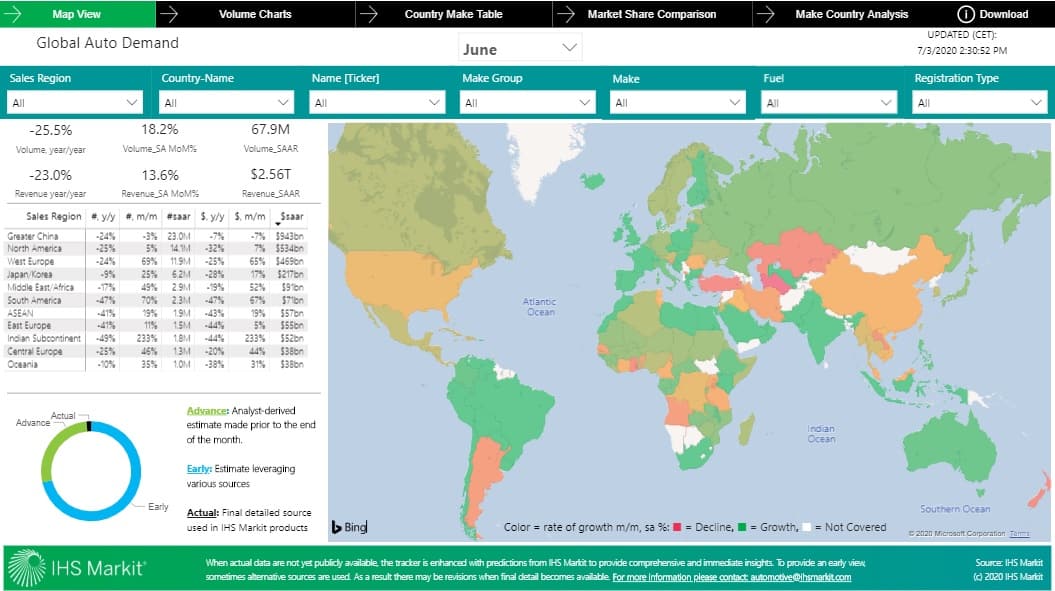

Customer LoginsGlobal Auto Demand Tracker - new sales/registration numbers for June 2020

Advanced estimates for June for 10 countries, on a month-on-month basis, show a further stabilisation of demand in a number of countries. Early results of the stimulus package resulted in France posting 1.3% y/y growth for June - a much-needed positive signal.

Despite positive short-term signals, it must be kept in mind that for the first half of the year, demand is almost halved from the prior year in Spain and Italy.

Furthermore, uncertainty surrounding the introduction of incentives in several markets is causing many private consumers to delay purchase decisions as they wait for government decisions. Early and clear messaging is required to avoid stagnation in many markets.

- In the United States, light-vehicle sales estimates for June showed a further drop in demand in the region of around 26% on a year-on-year (y/y) basis, although this represents an improvement compared to May, as incentives, online sales, and reopening of activities - especially at auto dealerships - supported sales. Vehicle sales are down around 23% y/y for the first half of the year.

- The pace of decline is easing and if we use China as an example of a market that is around six weeks ahead of many nations in the cycle, there are indications of a tenuous recovery.

- Europe again reported a sharp contraction in its key markets with Italy falling 23% y/y and Spain 36% y/y. Although these declines are not as steep as previous months, the continuing low volumes underline the challenging conditions in these post-COVID-19 virus lockdown markets. Factors include constricted supplies of vehicles, uncertainty in the tourism sector affecting rental fleets, and impending government support incentives leaving buyers delaying purchases.

- Registrations in Germany fell around 32% y/y in June, although this is a considerable improvement on the 61% drop witnessed in May. For the first half of 2020, year-to-date (YTD) sales were down nearly 35% y/y, although this still represents one of the better performances for Europe as a whole.

About the Global Auto Demand Tracker

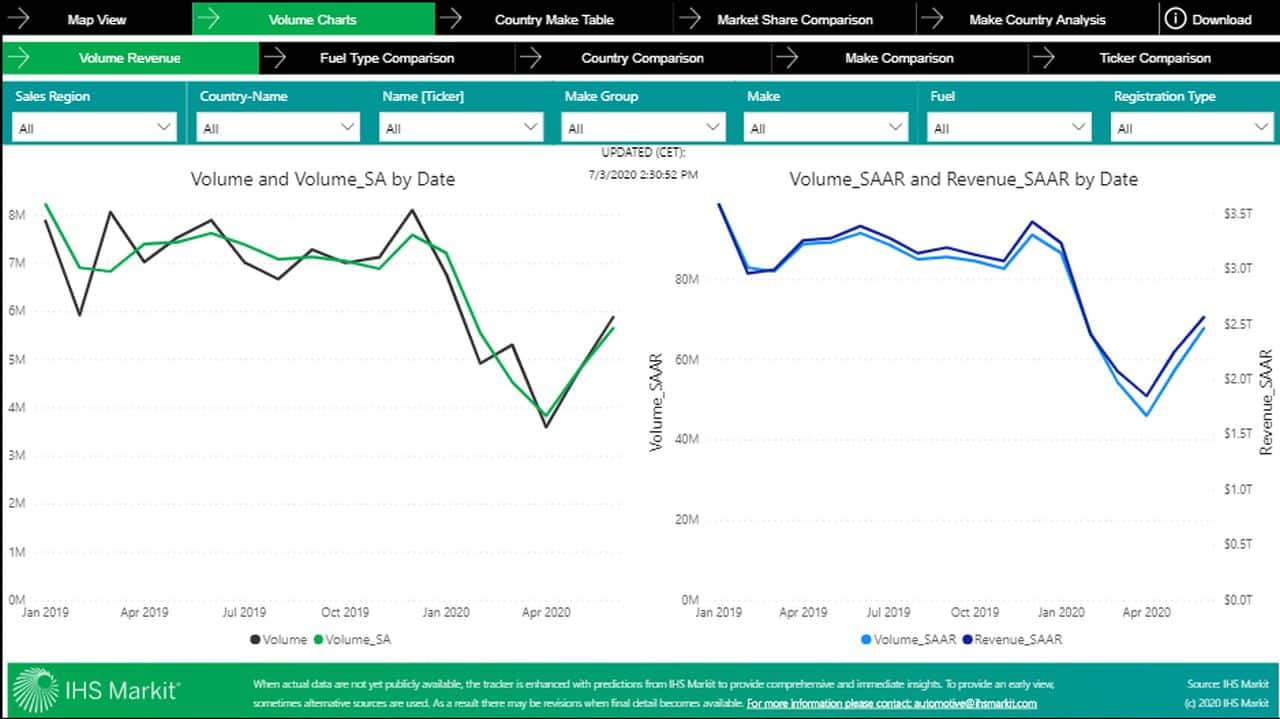

The Global Auto Demand Tracker is updated daily with sales and/or registrations by country by make for the most recent calendar month. Where an actual date is not yet publicly available, the IHS Markit Sales Operations prediction for the month is provided.

The Global Auto Demand Tracker allows automakers and their national sales arms to see which markets are sliding into crisis, which are emerging, and at the pace of the recovery. It also shows which brands are being hit the hardest in terms of volume and market share.

Access the Tracker on Connect. If you are not a subscriber to Connect, fill out the registration form and request a free trial to Connect.