Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

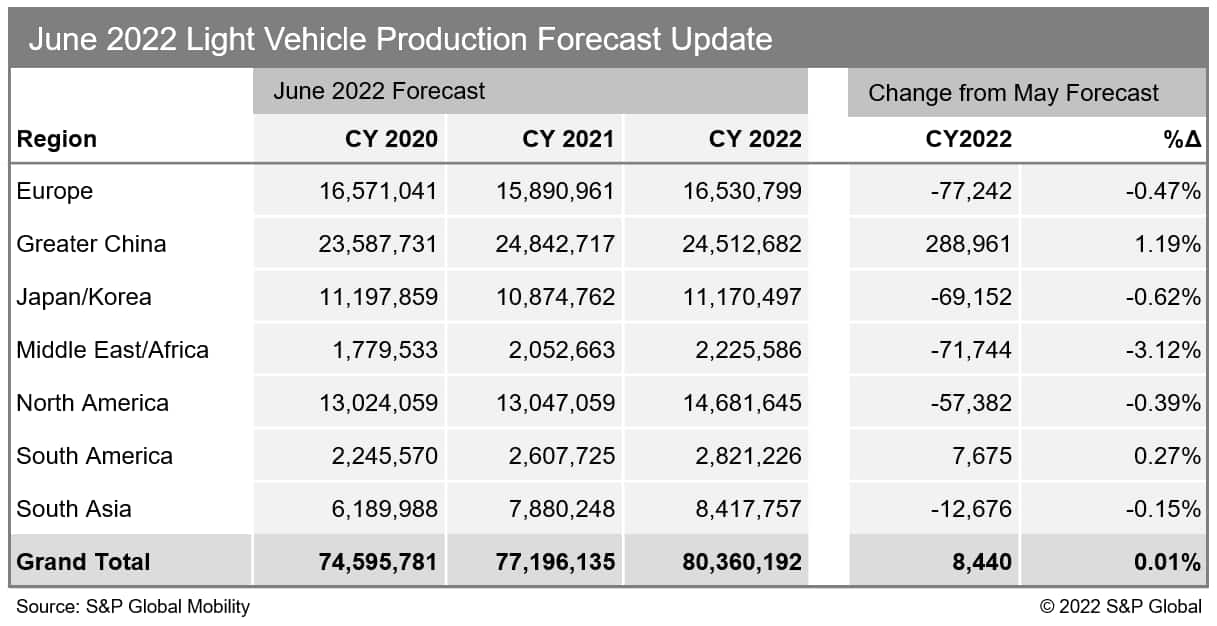

Customer LoginsS&P Global Mobility updates light vehicle production forecast for June

Production revisions continue to reflect the dynamic environment impacting the auto industry. The March 2022 forecast update resulted in a rather significant production realignment due largely to the Russia/Ukraine conflict. Since then, our team at S&P Global Mobility has done some "fine tuning" with this month's forecast update, which includes some more meaningful adjustments than others as COVID lockdowns in China impact the domestic market as well as some surrounding markets, and ongoing semiconductor supply conditions remain challenging for most automakers globally.

As COVID lockdowns in China are lifting and the government looks to stimulate auto demand, the profile for that market shifts to one of nascent recovery while other surrounding markets still cope with lingering supply chain dislocations due to the lockdowns in the near-term.

On the semiconductor front, mixed signals are apparent with some automakers reporting an improved supply of chips while other players still struggle with consistent supply of critical components. We remain watchful for potential demand destruction caused by slower economic growth forecasts for 2024 and beyond. The S&P Global Mobility June 2022 forecast update reflects a near-term increase for Greater China due to COVID lockdowns expiring and demand stimulus taking effect. Conversely, lingering supply chain impacts from the lockdowns in China result in downward revisions for Japan/Korea and South Asia and supply chain pressures continue to impact the near-term outlook for Europe and North America.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.