Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer LoginsWhat motor sourcing says about a carmaker’s electrification ethos

What motor sourcing says about a carmaker's electrification ethos

Incumbent automakers are grappling with a big dilemma: How fast to electrify their production capacity? And in so doing, whether to prioritize flexibility of powertrain type (given uncertain EV demand) or absolute scale? Furthermore, how do we know which such strategies the various automakers favor?

Making own electric drives demands heavier up-front investment

Automakers' decisions on 1) whether to build dedicated electric product architectures; and 2) whether to manufacture their own battery cells (or indeed assemble packs) are already quite well scrutinized. However whether they make or buy their own electric drive units (and in what ratio) is another enlightening metric. It is a particularly interesting one due to the spread of approaches among the major players.

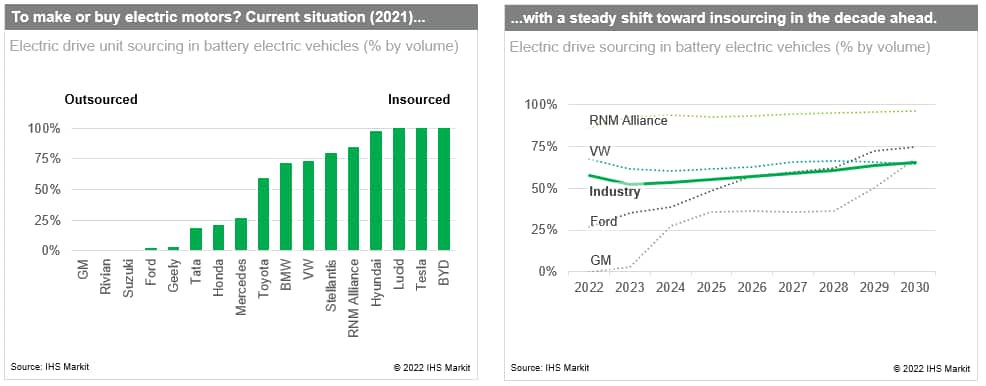

Established electric players prefer to make their own

Electric-only players tend to see electric drive units as vital to efficiency and thus a source of competitive advantage. The units comprise a high voltage inverter, the electric motor, and its transmission components. Tesla and Lucid designed and build 100% of their own and have been vocal about the benefits they achieve from limiting energy loss in the designs. Meanwhile many incumbent carmakers have started out sourcing drive units externally from Tier 1 suppliers like Bosch. In between there are a range of approaches. Hyundai (97%) and Renault-Nissan-Mitsubishi (85%) are already overwhelmingly insourced, while Ford (2%) and Honda (21%) are as of today largely outsourcing.

Tide shifting toward insourcing

We forecast a steady shift toward electric drive insourcing in the coming decade driven in part by the US OEMs. However, there will be many situations where outsourcing continues to make sense. For example, Rivian has initially fully outsourced its electric drive which helped accelerate its first product launch, while subsequently developing its own. BorgWarner's recently announced acquisition of motor supplier Santroll shows Tier 1s still see significant volume growth in this space. Carmakers may never insource electric drives completely. As mature as the internal combustion engine is, that industry is 90% insourced, while 10% of engines are externally sourced.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.